But there’s another side to those challenges that doesn’t get as much attention — the retirement savings gap.

If minorities are less likely to get an inheritance from a family member than a white person is, or to have wealth to fall back on when they want to buy a house or start a business, they are likely to have less money to save for retirement, too. And if they are saving, the weaker safety net makes it more likely that they’ll have to raid that reserve or take on debt when things go wrong.

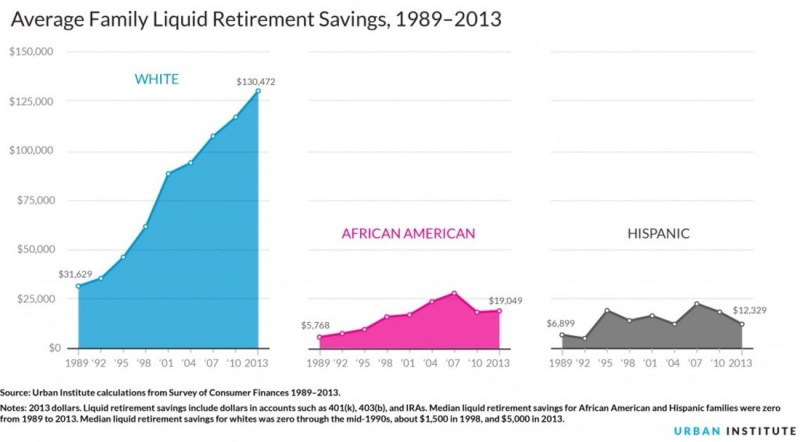

White families had over $100,000 more in average liquid retirement savings in 2013 than African American and Hispanic families, according to an analysis done by the Urban Institute, which released a series of charts illustrating wealth inequality in America. That difference has quadrupled over the past 25 years: In 1989, white families had $25,000 more in average retirement savings than minorities.

In terms of ratios, white families went from having five times the average savings held by minorities, to having between seven and 11 times the average amount of savings.

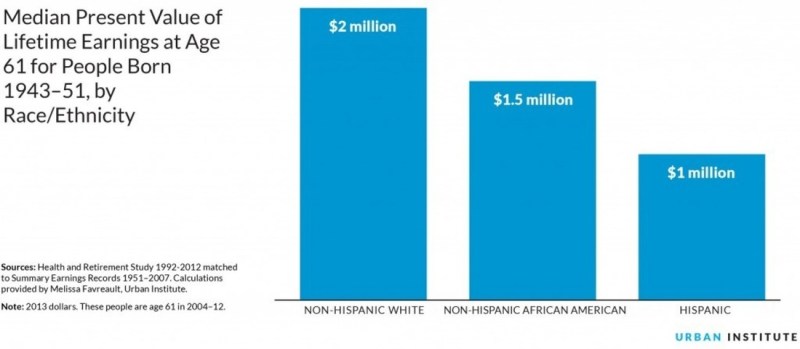

Take a look at income, for instance. Retirement experts often note — and rightly so — that minorities tend to earn lower wages than white families, leaving them with less disposable income to save. Indeed, the typical white person earns $2 million over a lifetime, compared to $1.5 million for the typical African American and $1 million by the typical Hispanic worker, the Urban Institute reports.

It’s hard to ignore how those jarring differences in earnings might create a setback, but the savings gap persisted even when researchers looked at workers with similar income levels. “We found that even after controlling for income and age, African American and Hispanic families have less,” says Signe-Mary McKernan, senior fellow and economist at the Urban Institute.

But participation rates alone don’t explain the savings gap, McKernan says. If they did, African Americans, who have saved an average of $19,000, would be closer to matching the average $130,000 saved by white workers. Instead, their savings are closer to that of Hispanics, who have put away an average $12,000 in retirement accounts, she says.

That suggests that some workers may be held back by other factors, such as how much they save and how they invest those savings, McKernan says. The latter is an issue my colleague Michael Fletcher has reported in the past: Even wealthy African Americans are much more conservative with their savings than whites with similar finances, investing more of their money in cash and savings bonds, and that could be limiting their investment growth.

So what should be done? Workers can start by increasing their savings rates and signing up for auto-escalation, which would up their contribution rates for retirement accounts by one or two percentage points each year until they reach a target savings rate. Some people may also want to evaluate their portfolios, and make sure they are not being too conservative with their savings.

Policies that make it easier for minorities to build wealth can help, McKernan says. As the institute points out in the post, white families have more wealth than African American and Hispanic families, and they are more likely to inherit a windfall from a relative. That support from family creates a cushion that prevents them from taking on debt or dipping into retirement accounts when emergencies happen, or even to cover planned expenses like co

llege, McKernan says.

The group recommends placing a cap on tax breaks like the mortgage interest deduction and using the difference to introduce a more generous credit for first-time homebuyers. It also suggest reforming some of the programs meant to help low-income families, which may discourage savings by disqualifying families with a certain amount of assets.

If more workers automatically enrolled workers in retirement savings plans, that might make it easier for people to save more consistently, McKernan says. And savings programs that encouraged people to set aside an emergency cash fund, such as a program that linked tax refunds to savings accounts, might prevent workers from tapping into their retirement accounts.

By Jonnelle Marte